If so then, it will make the Fed, whose primary function is converting government checks/debt into spendable credit, obsolete as the very act of deposit creates the credit to pay in one step. There is nothing to settle, the check is paid in full upon deposit, and any bank can do that. Banning cash would totally eliminate government debt. What would they owe? It’s already paid in full at the moment of deposit !!

What value would a Treasury Bond held by any bank hold? They would no longer be I.O.U. Cash Dollars, they would no longer represent a government debt obligation, as any ‘Promise To Pay’ by government, is paid the instant the banks used it to create credit, paid in full.

With credit as the de facto ‘Unit Of Account’, any credit created by banks using Government Bonds, would have to be returned to the government with the bond as that credit is a product of the bond and is attached to the bond throughout its existence. No bond, no credit. This transforms banks into the primary debtors, effectively reversing the rolls of obligor and obligee.

Those fools in the banking system who are promoting the banning of cash are totally outwitting themselves as it will make all centralized banking with its attendant government debt obsolete, and place the banks who use Treasuries to create credit, in debt to the government!

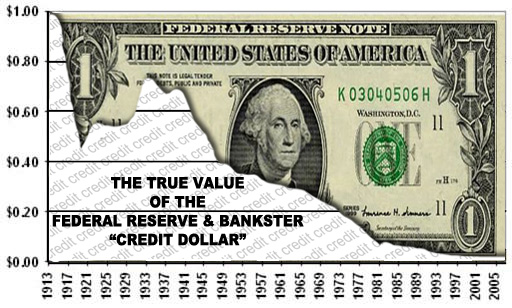

Also: If they ban the use of cash, that ban would have to be 100%, any less than that, and they leave in place a tool to measure the value of the credit in use, a means by which credit can and would be discounted. To give you an idea of that potential discount; if we were to properly value the 'credit dollar' against the current unit of account, the legal tender FRN, the true value of the bankster's fictitious 'credit dollar' would be around $0.03 in legal tender.

Note: 97% of the dollar's value has been stolen via the use of bankster generated debt/credit, erroneously referred to as 'dollars' and operating in the guise of 'our money'.

Wow......

Random Thought: The reason the QE's didn't work is simply due to the fact that it did not add any 'money' to the economy. It increased credit/debt but not the actual money supply. Credit, which is always someone else's debt, is channel locked, it cannot and does not flow the way actual, debt free, money flows, it is not dynamic. And new credit always has to be borrowed into economic existence. It is my contention that the economy is starved for the lack of free-flowing, debt-free cash.

Credit as currency is invisible, it does not provide the tangible, visible proof of quantity and it is this intangible, lack of proof of quantity that lets the government run up an $18-Trillion debt with little inflationary consequence. Can you just imagine the effects from $18-Trillion in Legal Tender Notes flooding the world? The dollar's value would have been crashed into a hyper-inflated mass, long before it reached $18-Trillion. Seeing is Believing.

Something to think about.....

See: The Ban on Cash - Part II

Submitted by: BarnacleBob

ReplyDelete@ Dibley… Seems to me that the chart exhibiting the collapse in the $ purchasing power is rather misleading as a benchmark… The physical dollar by soverereign decree of congress is valued @ 100 cents, same as it has always been since the first “coinage act” of 1792.

The physical unit is as you reference it LTM (legal tender money) supply, while the Austrians classify it as a component of TMS (true money supply)… regardless of the classification, the physical “cash & coin” in circulation IS the ONLY “legal tender” in circulation backed by the U.S. .Govs Treasury…

The remaining components are essentially “PRIVATELY” issued or held assets that merely play & more importantly ACT like true money to facilitate transactions in commerce within the private market… A bank cashiers check or money order is not money, it is a claim on physical money backed by the banks obligation to “exchange” their private credit for money that facilitates commerce in the private market…

The entire system is flooded with privately created bank credit and other representations & claims that are serving as proxy defacto monetary substitutes such as equities, corporate & sovereign bonds, etc… these serve as transferable values from one economic participant to another… and may be redeemed for a bank deposit entry and/or in currency upon demand.

Which brings us to discriminating between the True value of a SCARCE physical $ unit ($1.3 trillion in circulation) v. tens of trillions of dollar DENOMINATED PRIVATE CREDIT that is essentially created out of thin air “on demand” that circulates as the equivalent of an actual physical $ unit on account…

The so called proxy substitutes are valued at par initially under “THE” gold standard, and the Bretton Woods quasi gold standard… under these standards dollars & dollar denominated credit were redeemable in physical substance (gold), hence a dollar of every kind was as “good as gold,” redeemable thereof… Participants were confident in both the money and the credit issued upon the money due to it’s convertibility…

Understanding this is most important … these systems both collapsed when the volumes of credit issued far outstripped the ability of the issuers of gold denominated credit to honor the obligations of redemption in substance. The systemic over issuance of credit (inflation) caused the currency to lose purchasing power creating market price inflation in goods & services while the scarce gold backing actually gained purchasing power at the expense of the issued credit…

Today, in light of the fiat monetary system, the same event has happened… a tremendous over creation of credit has swallowed the scarce volume of physical LTM in circulation. The credit issued essentially possesses a true purchasing power of around $.043 cents ($4.3 cents) while the physical dollar remains @ 100 cents par… This means it is the CREDIT DENOMINATED IN $ that is loosing purchasing power parity, but not the physical unit itself. As noted above, the gold itself did not lose value relative to the credit, on the contrary it gained purchasing power… In this circumstance, it becomes axiomatic that the physical & scarce LTM should be gaining value to the inherent holders of the physical cash & coinage whilst the proxy $ substitutes should continue to devalue with the greater & greater volumes of credit issuances…

Needless to say, the players behind these schemes rely upon the populations ignorance of just how currency, coin & credit operate… It is dishonest, fraudulent & deceptive to present dollar denominated credit which is created & valued @ $ 4.3 cents as the equivalent defacto monetary until valued at a par of 100 cents… In this case, the dollar denominated credit issuers are skimming 95.7 cents from the debtors… What a deal! For the creditors …

Amazing thoughts! These are helpful for our mind concentration. Your Blog is so interesting.

ReplyDelete